Financial scams do not usually begin with something that looks ridiculous. The better ones look routine. A broker website. A trading app. A market analyst. A Telegram group. A crypto platform. A managed account. A bond offer. A recovery agent. A social media post from someone who appears to understand markets and has the screenshots to prove it, allegedly.

For traders and investors, scam risk is not separate from market risk. It sits in front of it. A trader can study charts, read macro data, manage position size and still lose money before a real trade happens because the broker, platform or adviser was fake. An investor can understand asset allocation and still be caught by a cloned firm selling bonds, private funds, crypto yield or structured notes that do not exist in the form advertised.

Market losses are part of trading. Scam losses are different. They usually come from false identity, false regulation, false performance, false withdrawal processes or false promises. The victim does not lose because the trade thesis failed. They lose because the trade environment was built to take deposits and block exits.

Resources such as Investing.co.uk can be useful for following markets, comparing financial information and researching trading topics, but every broker, platform, service or investment offer still needs independent verification. Reading about markets is not the same as verifying where client money is going.

The central rule is boring but useful: before sending money, identify the firm, check its authorisation, confirm its payment route, read the withdrawal terms and question any claim that sounds too clean. Scammers want speed, emotion and trust. Traders should answer with delay, evidence and paperwork. Not glamorous. Usually cheaper.

Why Financial Scams Work On Traders And Investors

Financial scams work because they borrow from real finance. The language is familiar enough to sound credible. Scammers talk about liquidity, arbitrage, copy trading, staking, hedging, private allocations, institutional signals, AI execution, market maker flow, managed accounts, high yield notes and structured returns. Some of these terms belong in legitimate finance. That is why they are useful to criminals.

The scammer’s job is not always to invent something new. It is to attach a real term to a false process. A real broker has a platform. A fake broker can have a platform. A real investment fund has documents. A fake fund can have documents. A real crypto protocol has wallets and contracts. A fake one can copy the language and add a wallet address.

The FTC’s investment scam guidance warns that investment scams often promise high returns with little or no risk. That remains the most reliable warning because genuine markets do not remove risk on command. A strategy can have an edge. A bond can have a coupon. A fund can have a track record. None of that means a stranger can promise steady large profits without downside.

Traders are especially vulnerable to urgency. They know opportunities can move quickly. A stock can gap. A currency can break. A token can run. An index can squeeze. Scammers use that knowledge against them. The message becomes: act now, join now, deposit now, upgrade now, recover now. Delay is framed as weakness.

That pressure matters because proper due diligence takes time. A person checking the legal entity, regulator, domain name, payment recipient, withdrawal terms and complaint history is harder to defraud. So the scammer turns time into a threat. The allocation is closing. The group is almost full. The bonus expires. The signal is live. The recovery window ends today.

Social proof adds another layer. A platform shows testimonials. A group chat shows profitable members. A creator posts withdrawal screenshots. A broker displays awards. A fake investment article quotes invented experts. None of this proves legitimacy. Screenshots can be edited. Reviews can be bought. Awards can be meaningless. Comment sections can be staged. The internet has made fake confidence cheap.

The SEC’s guidance on avoiding investment fraud tells investors to investigate independently and not rely only on information from the seller. That advice sounds painfully obvious, which is usually how the best fraud prevention advice sounds after the damage is done. The person selling the investment has no reason to correct your misunderstanding if the misunderstanding gets the deposit sent.

Scams also work because victims often hesitate to admit the problem. If a platform shows a large balance, the victim wants that number to become real. When the firm asks for another fee to withdraw, paying can feel like the final step. Often it is just the next step in the theft.

Fake Brokers And Cloned Platforms

Fake brokers are among the most damaging financial scams because they imitate the normal trading process. The trader opens an account, uploads documents, deposits funds, sees market prices, places trades and watches the balance move. The platform may look professional. Support may reply quickly. The account manager may sound calm. The problem often appears only when money needs to come back out.

The withdrawal stage is where many fake platforms reveal themselves. The trader requests a withdrawal, then receives a new condition. Tax clearance. Anti money laundering release. Account upgrade. Liquidity fee. Wallet verification. Margin repair. Settlement charge. Trading volume requirement. The trader is told the withdrawal is approved, but one more payment is needed. Then another.

Real brokers can charge fees and run compliance checks. They can request identity documents and delay withdrawals for valid reasons. But a broker demanding fresh deposits before releasing existing funds should be treated as a major warning sign. A valid fee can usually be deducted from the account balance under written terms. A scam fee is often payable separately because the balance on the platform is not real money in the first place.

Cloned firms are more subtle. A scammer copies a legitimate company’s name, logo, licence number, website style, staff names or address. The victim searches the name and finds a real firm on a regulator’s register. That creates confidence. The missing step is checking whether the website, phone number, email address and payment instructions match the official record.

The FCA’s Warning List helps UK consumers check firms the regulator has flagged as unauthorised, but absence from a warning list is not proof of safety. A new scam may not be listed yet. A cloned firm may use details that look close enough unless the victim compares them carefully.

In the U.S., investors can use FINRA BrokerCheck to research brokers and brokerage firms. This kind of checking matters because a fake broker may borrow the identity of a real professional or firm. The name alone is not enough. The official contact details and permitted activities matter.

Fake platforms often use account managers to increase deposits. The manager calls after account opening, explains trades, praises the trader and suggests larger funding. Early profits may appear on the screen. The trader may be allowed to withdraw a small amount. That does not prove safety. A small withdrawal can be bait used to encourage a larger deposit.

The fraud can also involve a real trading product sold through a fake venue. Forex, CFDs, crypto, binary options, options and commodities are real markets or instruments. A fake broker can still display them. The product label does not prove that trades are being executed, client money is segregated, or withdrawals will work.

The safest assumption is that any new broker is untrusted until verified. Not accused. Not guilty. Just untrusted. The burden of proof should sit with the firm asking for money.

Social Media, Signal Groups And Fake Authority

Social media has lowered the cost of building fake credibility. A scammer can create a profile, post market commentary, copy photos, buy followers, edit profit screenshots and move viewers into private messages. The public content may look like education. The private chat is often where the pressure begins.

Signal groups are a common route. The trader sees a post about profitable trades, joins a free Telegram, WhatsApp or Discord group, then watches members post wins, screenshots and praise. The group may push a specific broker, a paid tier, a copy trading account, a crypto token or a managed account. The room creates the feeling of consensus. Nobody wants to be the awkward person asking why the broker is registered in a jurisdiction nobody can pronounce.

The FINRA guidance on fraud red flags warns investors to watch for pressure and offers that seem compelling but carry hidden warning signs. Group environments make this harder because pressure can look like community. A trader sees other members acting quickly and assumes delay means missing out.

Fake authority is also common. Scammers impersonate analysts, brokers, educators, fund managers, lawyers, regulators and public figures. They may use a near identical username, stolen profile image or copied branding. A trader who follows a real market commentator may receive a message from a fake account offering private signals or account management. The real person has no involvement.

Social media also creates false proof. A profit screenshot is not audited performance. A video of a dashboard is not proof of custody. A withdrawal screenshot is not proof that all clients can withdraw. A luxury car is not a trading record. It is a car, sometimes rented, sometimes borrowed, sometimes irrelevant. Finance has enough nonsense without treating watches as due diligence.

The FTC reported that social media was involved in a large share of reported scam losses in 2025, with billions of dollars in reported losses connected to scams that started on social platforms. That makes social media a major risk channel, not a harmless side issue.

Trading education is not automatically suspicious. Some creators explain markets responsibly. The warning is about the move from education to funding. Once a creator pushes a broker link, private group, trading bot, account manager, token sale or paid signal service, traders should ask how the promoter is paid. Affiliate commissions, referral fees, spread sharing, course sales and token allocations all change incentives.

The phrase “not financial advice” does not make a misleading promotion safe. A video can still influence a viewer to deposit money, buy a product or follow a trade. A disclaimer does not verify performance, regulation or risk. It also does not refund losses, which is the part most people would prefer.

Social media is useful for finding ideas. It is a poor place to verify trust. Verification belongs with regulator registers, legal documents, payment checks, withdrawal terms and independent evidence.

Crypto Investment Scams And Payment Traps

Crypto scams deserve separate attention because crypto can be both the supposed investment and the payment method. A victim may be told to buy a token, deposit on an exchange, join a staking pool, trade through a private platform, connect a wallet or send funds to an address. Once funds move, recovery can be difficult.

The FBI’s cryptocurrency investment fraud guidance describes scams where victims are persuaded to send funds into fake investment platforms controlled by criminals. The platform may show profits, but the money is already under the scammer’s control.

A common structure begins with trust building. The scammer contacts the victim through social media, messaging apps, dating platforms, professional networks or wrong number texts. The conversation may not begin with finance. Over time, the scammer introduces an investment opportunity and offers to help. This makes the pitch feel personal rather than commercial.

Fake crypto platforms often show steady gains. When the victim asks to withdraw, the platform demands tax, gas fees, wallet validation, liquidity release, smart contract activation or anti money laundering approval. Some of these terms resemble real crypto mechanics, which makes them more convincing. But real words can still be attached to fake demands.

The FTC’s cryptocurrency scam advice warns that crypto investment scams often promise large profits with little or no risk and that crypto can be used as both the investment and the payment. That is the awkward part. The victim may think they are buying into a market opportunity while also using a payment method that is hard to reverse.

Wallet based scams work differently. The victim may connect a wallet to a malicious website, sign a harmful approval, reveal a seed phrase or install remote access software. Once control is granted, assets can disappear quickly. No legitimate exchange, broker, support agent or regulator needs a seed phrase. There is no clever exception hiding in the footnotes.

Crypto does not need to be banned from a trader’s life. It does need stronger personal controls. Traders should understand custody, wallet permissions, token liquidity, smart contract risk, exchange regulation, withdrawal rules and tax treatment before sending funds. Anyone who does not understand what they are signing should not sign it. The blockchain is not famous for customer support.

High Risk Instruments Used In Scams

Some financial instruments appear frequently in scams because they are complex, volatile or easy to market. The instruments themselves are not always scams. Binary options, CFDs, forex, crypto assets, structured notes, private placements, options and leveraged ETFs can exist legally and be used by experienced traders. The problem is how they are promoted and who is offering them.

Binary options are a good example. The product has a yes or no payout structure. It may be legitimate in specific regulated settings, but it has also been heavily associated with fraudulent platforms. The CFTC’s binary options fraud page says binary options can be traded on registered U.S. exchanges, while warning that many online platforms operate unlawfully.

CFDs and retail forex are also high risk because of leverage. A trader can control a large position with a small deposit. That can magnify profits, but it can also magnify losses. Scammers use this environment because losses can be explained as market volatility, margin requirements or spread changes. Sometimes the loss is real trading risk. Sometimes the platform was fake.

Structured notes and private placements are often sold with institutional sounding language. A product may promise fixed income, capital protection, asset backing or access to private opportunities. Some such products are legitimate. Others are unsuitable or fraudulent. The more complex the product, the more important it is to understand issuer risk, liquidity, valuation and legal rights.

Options and leveraged exchange traded products are real instruments, but they are not beginner shortcuts. The SEC’s investor bulletin on leveraged and inverse ETFs explains that these products are usually designed for daily objectives and may carry significant risks over longer holding periods. A product can be legal and still unsuitable for the person buying it.

The common theme is that high risk instruments require experience. Scams thrive when complex products are sold as easy money. If a seller makes a difficult product sound simple, the missing detail is usually risk.

Red Flags Before Sending Money

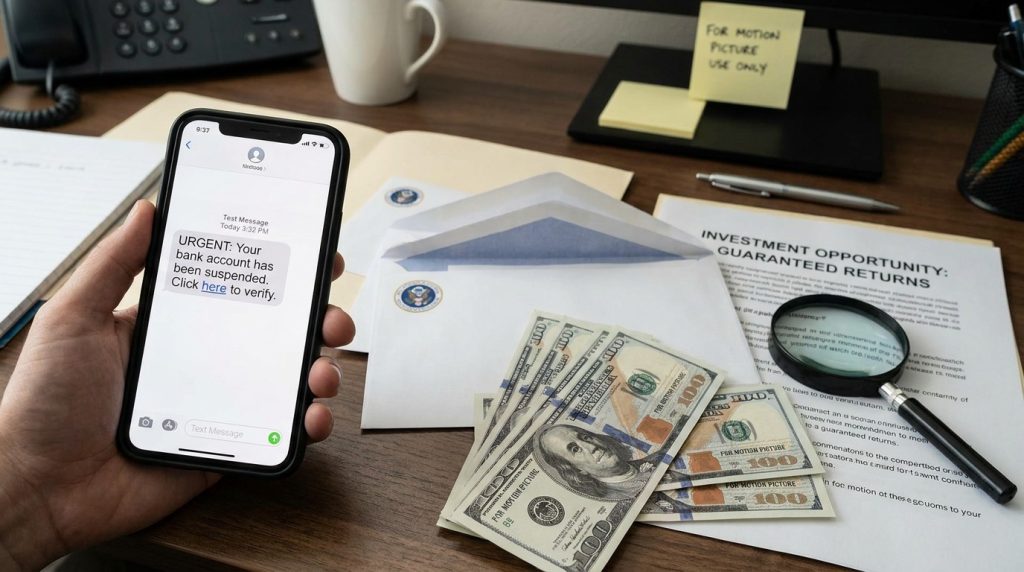

The first red flag is guaranteed return language. High returns with little or no risk should stop the process. Markets can produce large gains, but they do not provide guaranteed large returns to strangers through private chats.

The second red flag is urgency. Scammers push speed because checking takes time. The offer closes today. The broker bonus expires. The token lists soon. The account upgrade must happen before withdrawal. A trader should treat pressure as a reason to slow down, not speed up.

The third red flag is unclear regulation. A firm claiming to be licensed, certified, registered or globally approved should provide an exact legal entity, regulator, licence number and official register entry. Company registration is not the same as financial authorisation.

The fourth red flag is mismatched payment details. If the investment provider is one company but the payment recipient is another, the trader needs a clear explanation. Payments to personal accounts, unrelated businesses, payment apps, gift cards or unknown crypto wallets should be treated as high risk.

The fifth red flag is withdrawal friction. A platform that demands fresh payments before releasing funds is following a common scam pattern. Tax fees, release fees, wallet fees, liquidity fees and compliance fees often appear after the victim has already deposited.

The sixth red flag is secrecy. Scammers may tell victims not to speak with banks, advisers, family or regulators. They may say outsiders do not understand or that banks block profitable investments. This is isolation, not insight.

The seventh red flag is proof that proves nothing. Screenshots, testimonials, dashboard balances, luxury photos and comment threads are weak evidence. They can be staged or edited. Verified records, official registers, audited statements and clear legal documents are stronger.

The eighth red flag is remote access. A broker, adviser, exchange support worker or recovery specialist should not need full control of a customer’s device. Remote access can expose bank accounts, email, passwords, identity documents and crypto wallets.

The ninth red flag is emotional manipulation. The scammer praises the victim for acting quickly and criticises hesitation. They call caution fear. They call questions negativity. Real professionals answer questions. Scammers punish them.

The tenth red flag is recovery promises after a loss. Anyone promising guaranteed recovery for an upfront fee may be running the second scam. Fraud victims are often targeted again because criminals know they want the loss reversed.

Due Diligence Before Trusting A Firm

Start with the legal entity. The name on the website is not enough. A brand may have several companies under it, and protections may differ by jurisdiction. The account agreement and payment instructions should identify the actual entity.

Check the regulator. Use the official register, not a link supplied by the salesperson. Compare the firm name, licence number, permissions, website, phone number, email address and physical address. Similar is not enough. Clone firms rely on details being almost right.

Check whether the firm is authorised to offer the product being sold. A company may be registered for one activity but not permitted to provide trading services, investment advice, derivatives or crypto products to retail clients. The question is not only whether the firm exists. It is whether this entity can legally offer this product to you.

Read the withdrawal terms before depositing. Traders often focus on spreads, leverage, platforms and markets. None of that matters if funds cannot be withdrawn. Review fees, processing times, identity checks, bonus restrictions, dormant account charges and any conditions that can delay withdrawals.

Check the payment route. The beneficiary should match the legal entity or a clearly disclosed custodian or payment processor. If funds are sent to an unrelated company, individual or crypto wallet, the risk rises sharply.

Ask written questions. Who regulates the firm? Where are client funds held? Are funds segregated? How does the firm make money? What fees apply? How are complaints handled? How do withdrawals work? A legitimate firm should answer clearly or point to formal documents.

Search for warning patterns. Reviews are imperfect, and some are fake, but repeated complaints about blocked withdrawals, pressure calls, surprise fees, account managers and changed domains should not be ignored.

Finally, give decisions time. Scams dislike delay because delay allows evidence to catch up. If an opportunity cannot survive a day of checking, it probably should not receive capital.

What To Do After Suspected Fraud

If fraud is suspected, stop sending money. Do not pay release fees, tax fees, verification charges, account upgrades or recovery fees. A scammer asking for one more payment is not resolving the issue. They are testing whether the victim is still paying.

Save evidence immediately. Take screenshots of the website, account dashboard, balances, trades, chats, emails, phone numbers, names, payment instructions, wallet addresses, transaction hashes, bank details and identity documents sent. Export messages where possible.

Contact the bank, card provider, exchange or payment service used. Ask whether the transfer can be stopped, recalled, disputed, frozen or flagged. Crypto transfers are harder to recover, but fast reporting may still help if funds pass through a compliant exchange.

Report the matter through official channels. U.S. victims can report internet enabled fraud through the FBI Internet Crime Complaint Center, securities concerns through the SEC complaint process, broker related issues through FINRA’s complaint process, and consumer fraud through the FTC fraud reporting portal. UK victims can report suspicious financial firms through the FCA scam reporting page and fraud through Report Fraud.

Tell someone trusted. Scams feed on embarrassment and isolation. A second person can help stop further payments and spot follow up recovery scams.

Final Warning

Financial scams work because they make false trust look normal. They borrow real market language, real product names, real regulator references and real trading interfaces. The victim sees finance. The scammer sees a deposit.

A real firm can be verified. A real investment can explain risk. A real broker can answer in writing. A real withdrawal process does not require endless fresh payments.

Traders and investors already face enough uncertainty from markets. Scam risk offers no upside. Slow down before funding anything. Check the firm, regulator, payment route and withdrawal terms. The boring work before a deposit is often the money saving part.